NatWest suffered the biggest share price drop since the Brexit vote yesterday, wiping billions off the lender’s value as savers moving to higher interest rate accounts.

NatWest reported ‘disappointing’ third-quarter results, missing analyst profit expectations and trimming its lending margins guidance in a sign that the benefits of soaring rates have peaked.

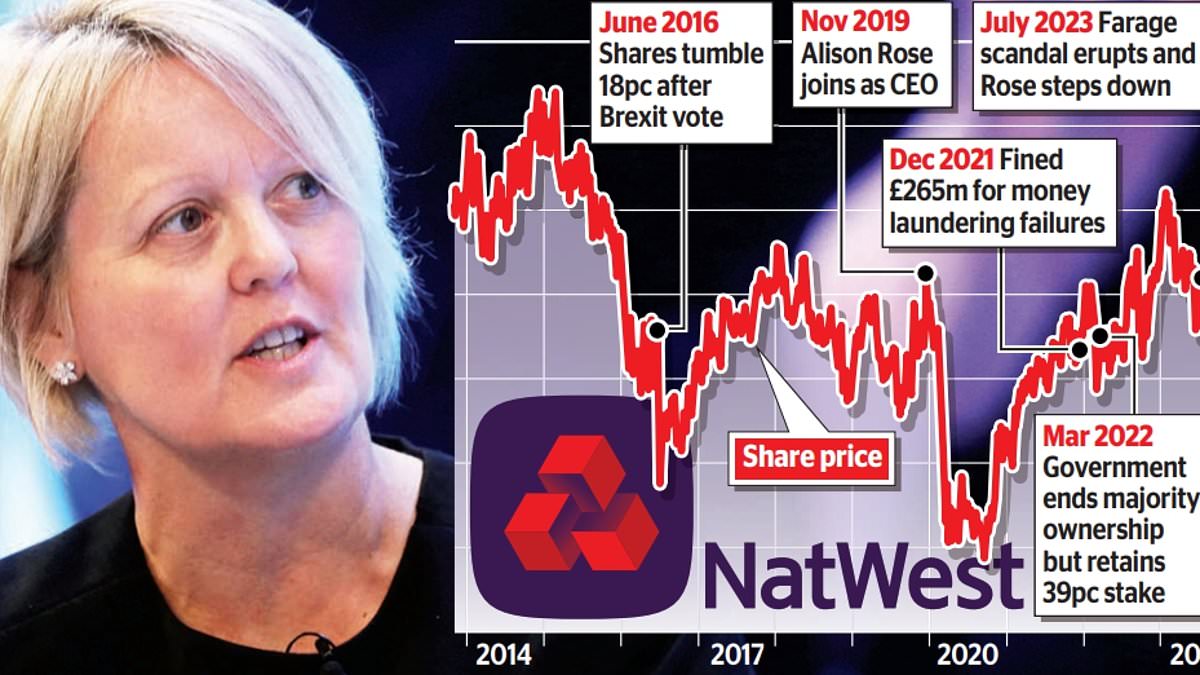

Shares tumbled as much as 18 per cent yesterday morning in their biggest dive since Britain voted to leave the European Union in June 2016, before paring earlier losses to trade down around 11 per cent.

NatWest shares closed at 182p, down 11.6 per cent, or 23.8p, knocking around £2billion off its market capitalisation. The slide cost the taxpayer £780m as the bank is still 39 per cent publicly owned following a government bailout in the 2008 financial crisis.

Analysts warned the fall could cause ministers to pause plans to sell off more shares in the immediate future.

Disappointing: Shares have been on a rollercoaster ride during Alison Rose’s troubled tenure

It came as NatWest, which also owns RBS and Ulster Bank, published the findings of an investigation into the closure of Nigel Farage’s Coutts account, with the City watchdog launching a review of the firm.

The scandal sparked a probe by the Financial Conduct Authority watchdog and forced ex-NatWest boss Dame Alison Rose to resign.

The report found the account closure to be ‘lawful’, as the bank’s relationship with Farage was ‘significantly loss-making’. But the bank failed to communicate properly and mishandled Farage’s complaint.

Banks have benefited from higher rates, which stand at 5.25 per cent, as they increase the amount of interest customers pay on mortgages and loans.

But experts said the benefits may have peaked as consumers switch to accounts with better savings rates, putting pressure on lenders’ margins.

NatWest said its net interest margin (NIM) – a measure of the difference in what it pays out in deposits and what it generates in loans – fell to 2.94 per cent as more customers moved to higher rate savings accounts.

It downgraded its NIM forecast for the year from 3.2 per cent to 3.15 per cent, based on the assumption that the Bank of England holds rates for the rest of 2023. Economists expect the central bank to leave the base rate unchanged next week.

Rival Barclays also downgraded its NIM expectations this week, sending bank shares spiralling.

Richard Hunter, head of markets at Interactive Investor, said: ‘The disappointing themes which have plagued bank results have unsurprisingly been echoed at NatWest, although perhaps to a lesser extent.

‘NIM declines across the sector have taken a toll on share price performance, while also suggesting that the benefits of higher interest rates have peaked as customers seek higher returns on their cash.’

He added that the share price decline is unlikely to alter the Government’s plan to sell its NatWest stake but ‘it could hold fire in the immediate future’.

NatWest profits were up 23 per cent to £1.33billion in the quarter, compared with £1.09bn the year before, but it fell short of the £1.36billion expected by analysts. Total income increased 8 per cent to £3.5billion.

It reported a net impairment charge of £229m, reflecting ‘low and stable’ levels of loan defaults, beating its competitors.

Chief executive Paul Thwaite said: ‘The results show that NatWest is a strong bank which is performing well, generating sustainable profits and returns.

‘Credit losses and impairments remain low and we are ready and able to stand by our customers and businesses.’

DIY INVESTING PLATFORMS

AJ Bell

AJ Bell

Hargreaves Lansdown

Hargreaves Lansdown

Interactive Investor

Interactive Investor

EToro

EToro

Bestinvest

Bestinvest

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence.

Compare the best investing account for you